Data●●Solid

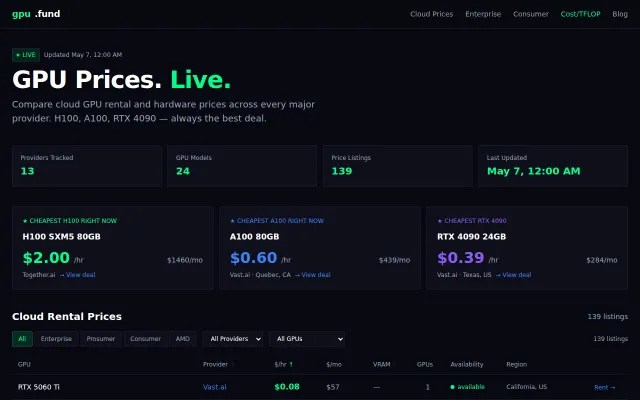

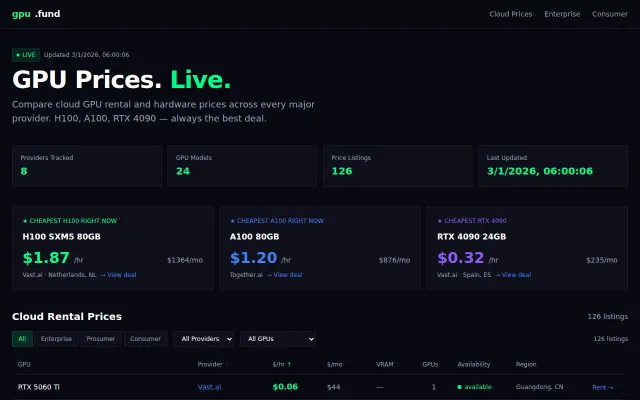

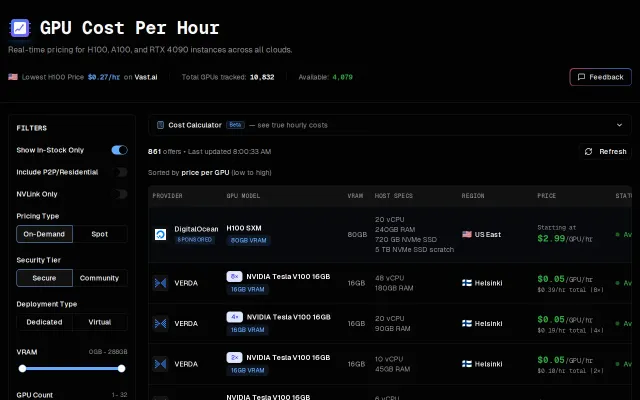

Daily GPU rental prices across 25 marketplaces

Finally, a Kayak for GPU rentals when Vast.ai and RunPod data is scattered.

Solve My Problem

AIMC

3028d ago

An index tracking realtime GPU rental prices and a perpetual futures marketplace that trades it

GPU derivatives with real funding rates and mark pricing—fills a genuine infrastructure hedging gap.

ML labs, cloud operators, quantitative traders, GPU rental marketplaces seeking compute cost hedging.

Hyperliquid (perpetual futures interface) · dYdX (derivatives platform template) · Vast.ai (GPU rental marketplace)

The idea is airlines hedge jet fuel, starbucks hedges coffee beans - as GPU compute becomes critical infrastructure the same hedging tools should exist. Not sure if anyone actually needs this but it was interesting to build.

How it works: - Pulls live H200 spot prices from Vast.ai every 15s into a tradeable index - Full perp mechanics: funding rates, mark price calc, real-time P&L - Event-driven Rust backend with supervisor pattern and circuit breakers - Next.js frontend with TradingView charts, real-time WebSocket updates

What's real vs simulated: - Real: Index construction, funding rate engine, forward curve, state persistence - Simulated: Order book depth and trade matching (its a single-client demo)

The backend is the part I'm most proud of - isolated tasks coordinated by a supervisor, each has it's own state machine so if one component fails it doesn't take down the others. Tried to build it with production patterns in mind even though its just a demo.

Also made a 15-page derivatives pricing doc that covers the economic model and hedging scenarios. Basically: rental prices = f(CAPEX, utilization, depreciation) so futures pricing reveals market expectations about GPU supply/demand.

GitHub: https://github.com/zacharyfrederick/compex

Would love feedback on the architecture or if the market mechanics actually make sense. First time building something like this.

Finally, a Kayak for GPU rentals when Vast.ai and RunPod data is scattered.

Finally a single tab to check H100 prices instead of opening ten provider dashboards.

Finally, an actual order book for GPU hours instead of a static listing wall.

Real-time GPU pricing comparison table, but Vast.ai's own UI does this natively.

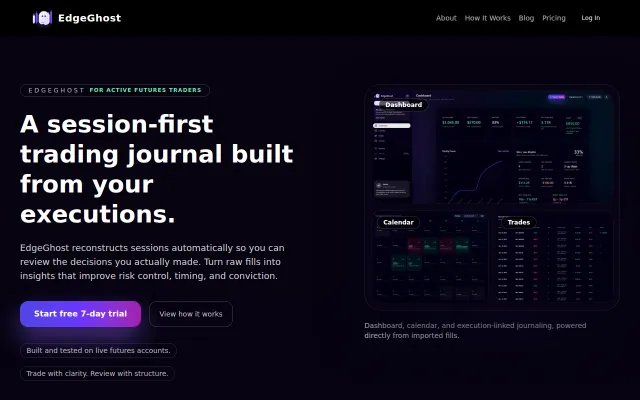

Execution-log reconstruction beats TradeZella's manual entry for futures traders.

It normalizes messy provider offers into a single table with filters for VRAM, NVLink, on‑demand vs spot, and 'in‑stock only' — exactly the controls you want when hunting GPUs. The UI is clear and fast (filters, region/provider lists, a cost calculator beta), but underneath it's still an aggregator with affiliate ties and scraping cadence risks, so expect to verify prices on the provider before launching.